Engine, not Edge: Five Quant Capabilities that Every Wealth Firm Needs

AI will turn quant from a specialist function to standard infrastructure for wealth management

Here’s a joke the Chief Investment Officer of a multi-family office once told me: “What’s the easiest way to spot an advisor with a small book of business? They have a Bloomberg Terminal.”

The joke works because it’s true. Success in wealth management isn’t built on stock picking or fancy data feeds. It’s built on trust - on showing up for clients, understanding their lives, and making them feel like their money is in good hands

But here’s the thing: advisors that can speak quant fluently - that can explain why a portfolio is constructed the way it is, what’s driving performance, where the risks are - build trust faster and deeper than someone who is just good at playing golf.

The problem isn’t that wealth firms don’t understand this, but that doing it rigorously requires access to quants - and quants are expensive. Family offices typically spend 0.5-1.5% of assets under management on operating costs, with staffing alone consuming 50-60% of that budget1. In a business where every basis point matters, firms need to be ruthlessly discerning about when they justify that cost.

Most firms do what makes economic sense: they use model portfolios or build portfolios by feel, explain performance in broad strokes, and hope nothing breaks. This works most of the time - until the one week it very much doesn’t, when markets break in unexpected ways or a client digs in on the one question you can’t answer cleanly in a proposal meeting.

The Category Error

The problem with most conversations about “quant in wealth management” is that they treat quantitative methods as one undifferentiated thing when they’re actually solving two completely different problems.

Quant as edge: systematic strategies designed to beat the market, aka a capacity-constrained space where dozens of well-capitalized systematic managers are mining the same alternative data sets for increasingly marginal improvements in Sharpe ratios. Think Renaissance Technologies, AQR, Citadel - this is where the big systematic shops live.2

Quant as engine: not about outperformance, but about rigor, transparency, and making sure that every unit of risk in a portfolio is rewarded with an appropriate amount of return. It’s the difference between “I think this looks balanced” and “I can show you exactly what you’re exposed to and why.”

Most wealth managers have no reason to compete on edge, but every firm should be using quant as engine.

What Quant as Engine Means in Practice

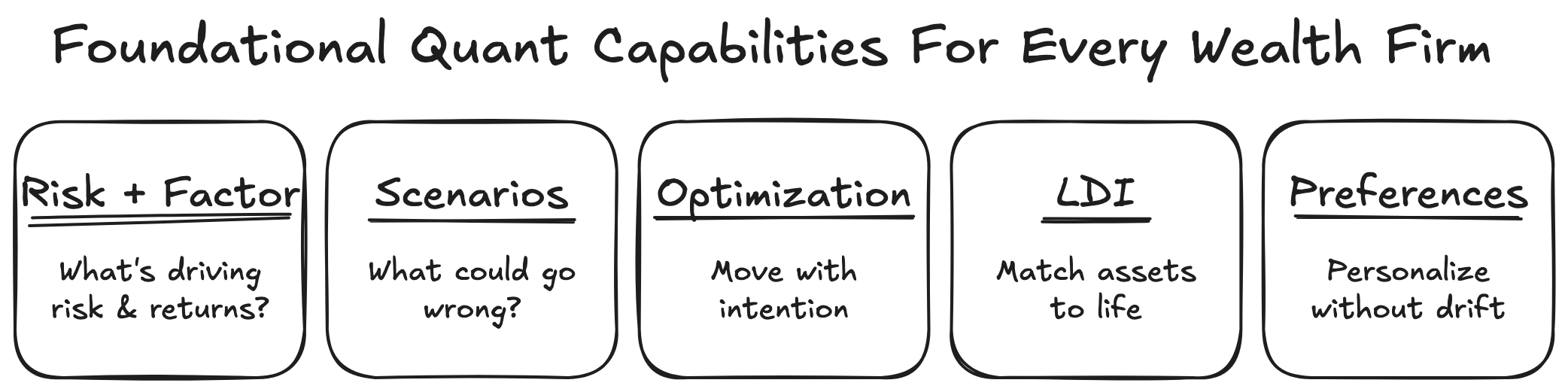

Every wealth management firm should be able to deploy five foundational quantitative capabilities. These aren’t about beating the market - they’re about understanding what clients own, building something intentional, and making it personal. Here’s what that looks like in practice:

1. Risk and Factor Analysis - Understanding What the Client Owns

Risk and factor analysis decomposes portfolio returns into their underlying drivers -market beta, sector exposure, factor tilts like value vs. growth, interest rate sensitivity. It’s the application of Markowitz’s modern portfolio theory’s insight3 that returns come from systematic exposures, not stock picking.

Most advisors can tell a client “stocks went down.” Far fewer can explain whether it was duration risk, sector concentration, or a factor rotation. When markets dropped in 2022, was it tech exposure, growth tilt, or simply beta? The difference matters because clients who think they’re diversified often aren’t - they’re running concentrated factor bets they don’t understand.

An advisor who can decompose performance - ”you lost 8%, the market lost 12%, and your value tilt plus lower duration cushioned the blow” - isn’t performing theater. They’re demonstrating that every position in the portfolio exists for a reason, and that reason held up when it needed to. That’s how an advisor builds trust through transparency rather than hoping nothing breaks.

2. Scenario Analysis - Preparing for What Could Go Wrong

Scenario analysis goes beyond generic Monte Carlo simulations to model specific, concrete outcomes that clients actually worry about: rate shocks, sector rotations, drawdowns comparable to 2008 or 2022. But the real value isn’t in the headline number - it’s in understanding the correlation breakdowns, the second-order effects, and which positions actually provide diversification under stress versus just looking diversified on paper. For sophisticated clients - founders with concentrated positions, families with complex estate structures, or portfolios mixing public and private assets - this extends to modeling liquidity cascades, cross-asset contagion, and scenarios where seemingly unrelated positions become correlated precisely when you need them not to be.

This isn’t about prediction - it’s about preparation. The underlying math reveals correlation breakdowns under stress, second-order effects across asset classes, and which positions actually provide the diversification clients think they have.4 Most clients don’t engage with abstract probability distributions. They engage with concrete scenarios that map to their actual anxieties.

An advisor who can show what breaks and what holds under stress - and has a playbook ready if any scenario materializes - isn’t just managing portfolios. They’re managing the client’s ability to stay invested when markets turn ugly. That’s especially valuable for clients with concentrated positions who need to see exactly what they’re exposed to before deciding whether to diversify.

3. Portfolio Optimization- Building Something Intentional

Portfolio optimization has a bad reputation because people associate it with Markowitz’s mean-variance models that implode when you adjust one input.³ But constraint-based optimization - respecting real-world limitations like taxes, liquidity needs, position minimums, and rebalancing costs - ends up being a lot more usable.

The goal isn’t chasing the theoretical efficient frontier. It’s answering: given where this client is today, where could they be with minimal disruption, and what are they giving up by staying put? Most portfolios aren’t optimized at all. They’re whatever the investment committee blessed, plus whatever the client brought from their last advisor, plus tactical tilts from three years ago that nobody remembers making.

An advisor who can visualize where a client sits on the risk-return spectrum and show what deliberate repositioning looks like isn’t just building better portfolios, but they’re demonstrating that every decision was intentional and not accidental. And that gap between intentional vs. accidental shapes more outcomes than most advisors think.

4. Liability-Driven Portfolio Construction - Matching Assets to Outcomes

Liability-driven investing (LDI) - standard practice in pension funds for decades5 -remains criminally underused in private wealth. Every client has liabilities: college tuition in six years, a home purchase, retirement income starting at 65. Most advisors build a “growth portfolio” or “income portfolio” and hope it lines up. I’ve seen advisors build elaborate financial plans - college funding, retirement income, estate goals - only to implement them with portfolios that barely differ from a standard 60/40.

The gap between planning and implementation is where LDI lives. It explicitly matches assets to future cash flows, stress-tests the probability of meeting specific goals, and shows what happens when timelines or amounts shift. Duration matching, goal-based bucketing, immunization strategies - these aren’t theoretical constructs. They’re tools for aligning portfolios to real life.

An advisor who can say “this bucket funds your daughter’s college, this one protects your retirement floor, this one is growth capital where we can take risk” is wrapping a narrative around quantitative rigor. When clients see that their actual financial outcomes - not just abstract returns - are being managed deliberately, the conversation shifts from performance anxiety to outcome confidence.

5. Preference Integration - Personalization Without Breaking It

Clients want portfolios that reflect their values6 - avoiding certain sectors, tilting toward themes, expressing conviction on specific issues. Most firms bolt this on clumsily, creating unintended concentrated bets or dramatically increasing tracking error without quantifying the cost.7

The rigorous approach treats preferences as constraints within an optimization framework: tilt toward client values while maintaining reasonable factor exposures and acceptable tracking error to a sensible benchmark. The advisor isn’t pretending customization is free - they’re making the trade-offs explicit and letting the client decide what they’re willing to pay.

Say a client wants to avoid pharmaceutical companies due to personal beliefs. A naive approach would excludes pharma tickers like JNJ 0.00%↑, PFE 0.00%↑ ,and MRK 0.00%↑ and move on. The rigorous approach shows the resulting sector tilts (likely overweight tech, underweight healthcare), the impact on expected returns and volatility (maybe 20-40bps of tracking error), which other positions need to rebalance to maintain market-like exposure, and whether this creates unintended factor bets. When clients see the actual cost - not in moral terms but in portfolio terms - the conversation becomes substantive rather than performative.

The Data Problem

At this point you might be thinking: well that’s nice, but this assumes clean, complete portfolio data - which is hilariously optimistic for wealth management.

Fair. The data problem is real. In systematic shops, quants have access to a proper securities master, subscriptions to Bloomberg and FactSet and Refinitiv, and have prime brokers with clean feeds. In wealth management, advisors work with PDF statements, missing cost basis, and private positions with no public pricing.

My response to such concerns is that the solution isn’t to demand perfect data before running any analysis - it’s to use reasonable proxies, be transparent about assumptions, and focus on insights that are robust to data imperfections. For liquid securities with missing history, synthetic returns can be generated based on asset class and factor characteristics. Private positions can be model as comparable public securities with appropriate liquidity and concentration adjustments. Factor exposures don’t change because of missing cost basis data. Correlation breakdowns under stress scenarios don’t disappear because you’re estimating a private equity position’s beta. The insights that matter for client conversations - “your portfolio has 30% more tech exposure than you think” or “in a 2008-style drawdown, these three positions all decline together” - are robust to reasonably bad data.

In wealth management, being directionally right beats being academically right. And directionally right with quantitative rigor beats pure intuition every time.

The Economics Are About to Flip

Right now, these capabilities I described above are expensive. A quantitative analyst costs $140,000+ annually - before benefits, infrastructure, and data subscriptions.8 Most firms can’t justify hiring quants or paying for point solution software that won’t directly generate revenue. That economic calculus is about to shift.

That calculus changes when quantitative rigor becomes infrastructure instead of headcount. AI is finally making the underlying architecture possible.9 I’ve written before that wealth management needs an operating system, not another tool. The shift isn’t about AI replacing advisors or generating alpha from black-box models. It’s about building infrastructure that makes this level of quantitative rigor something every advisor taps into without having to prompt explicitly.

The AI-native operating system for wealth management will be quantitatively rigorous under the hood, radically simple on the surface, and designed to make advisors better at having qualitative conversations. The quant layer is invisible in the day-to-day, but shows up when meeting prep automatically flags that a client’s tech concentration drove last quarter’s underperformance, or when a newsletter draft includes scenario stress tests customized to each recipient’s portfolio. Factor analysis, scenario testing, and liability-driven construction won’t be specialist knowledge locked behind a quant team - they will be baseline capabilities built into how advisors operates. So instead of having a quant on staff to run factor analysis for 50 clients or paying a service provider per-analysis, firms will have software that simply integrates that same analysis into meeting prep, proposal generation, and other workflows for all of their clients - at a fraction of the per-client cost.

The firms that adopt this infrastructure now - that treat quant as engine, not edge - won’t just get incremental efficiency gains. They’ll operate with a level of confidence most firms simply don’t have today. Their advisors won’t have to hope a model portfolio holds up or explain performance with hand-waving. They’ll know exactly what’s driving returns, where the risks sit, and what happens under stress. That confidence is the difference between hoping the portfolio holds up and knowing exactly why it will. Clients will notice.

Thanks for reading. If this resonated, feel free to share it with anyone working in wealth management or thinking about how the industry is changing in the age of AI.

Unstructured Returns covers the intersection of startup, AI, finance, and the systems that sit underneath them. If you’d like future pieces to land directly in your inbox, consider subscribing.

According to Citi’s 2025 Global Family Office Report and Goldman Sachs research, approximately two-thirds of family offices spend at least 0.5% of AUM annually on operations, with staffing representing the largest line item. For a detailed breakdown, see The Brutal Cost of Running a Family Office by Mr Family Office (link).

Didier Lopes and Alex Izydorczyk have both written sharp pieces on AI in hedge funds in response to Ken Griffin’s remark that “AI fails to help hedge funds produce alpha” that I recommend checking out. The tl;dr is that it’s not because the technology isn’t capable, but because firms haven’t built the unified data infrastructure that lets humans and AI actually collaborate. Wealth management faces a parallel problem with a different goal: not uncovering hidden alpha, but demonstrating that every decision was intentional and every outcome was managed deliberately. That requires the same foundation - connected data, systems that understand relationships, context that flows across domains. See Didier’s “Why generative AI isn’t uncovering alpha yet“ and Alex’s “Skepticism, early trends, and an early AI/quant taxonomy“ for their take on the hedge fund side.

Harry Markowitz (1952): Portfolio Selection, The Journal of Finance 7, no. 1, pp. 77-91 (PDF) Markowitz received the Nobel Prize in Economic Sciences in 1990 for this work, which established the mathematical foundation for modern portfolio theory.

For a comprehensive treatment of scenario analysis and stress testing in portfolio management, see Rebonato, Riccardo and Alexander Denev (2014): Portfolio Management under Stress: A Bayesian-Net Approach to Coherent Asset Allocation, Cambridge University Press (on Amazon). The framework has become standard practice in institutional risk management following the 2008 financial crisis.

Liability-driven investing emerged from actuarial science and pension fund management. For the foundational framework, see Sharpe, William F., and Lawrence G. Tint (1990): Liabilities - A New Approach, Journal of Portfolio Management 16, no. 2, pp. 5-10 (PDF). The approach is standard in institutional portfolios but remains underadopted in private wealth despite obvious applications.

Identity-expressive behavior, where investors make decisions that are irrational from a portfolio perspective but align neatly with how they see themselves, shows up in all kinds of ways beyond ESG and value tilts. Meir Statman has written about this expressive side of investing, and I’ve seen portfolios overweight with RACE 0.00%↑ because they own a Ferrari 308, or holding outsized positions in EOG 0.00%↑, DVN 0.00%↑, and NOV 0.00%↑ because they grew up in oil country.

The challenge of implementing values-based investing without unintended consequences is explored in Plantinga, Auke, and Bert Scholtens (2021): The Financial Impact of Fossil Fuel Divestment, Climate Policy 21, no. 1, pp. 107-119 (PDF). They find that naive exclusion strategies often increase concentration risk and tracking error more than investors expect.

According to Indeed, the average base salary for a quantitative analyst in the United States is $143,367 annually, with significantly higher compensation in major financial centers - Glassdoor reports averages exceeding $200,000 in New York. Benefits typically add 25-30% on top of base salary for health insurance, 401(k) matching, and payroll taxes. Data subscriptions add further costs: a FactSet workstation runs approximately $12,000-15,000 per year per seat, while a Bloomberg Terminal costs roughly $24,000-27,000 annually. For a mid-sized wealth management firm adding a single quantitative analyst with full infrastructure support, all-in costs easily exceed $200,000 annually - before accounting for office space, management overhead, recruiting costs, etc.

This is what we’re building at my startup Shatterpoint. Here is an early demo that shows how we’re ingesting a portfolio holdings document, then run a risk- and factor analysis over the portfolio, and present results in ways that advisors can actually use. We work with forward-thinking RIAs, multifamily offices, and wealth management firms that see AI not as hype, but as infrastructure for the next generation of advice. If this resonates, reach out - I’d love to compare notes.

That’s an interesting joke…