The Missing Layer - Part 1: Fragmentation

Wealth Management Needs an Operating System, Not Another Tool

This is the first of two essays on why wealth management’s technology stack is breaking - and what comes after it. In Part 1, I trace how fragmentation and “context loss” emerged and why the next generation of AI will force a rebuild from the ground up. Part 2 will look at what that new architecture might actually look like.

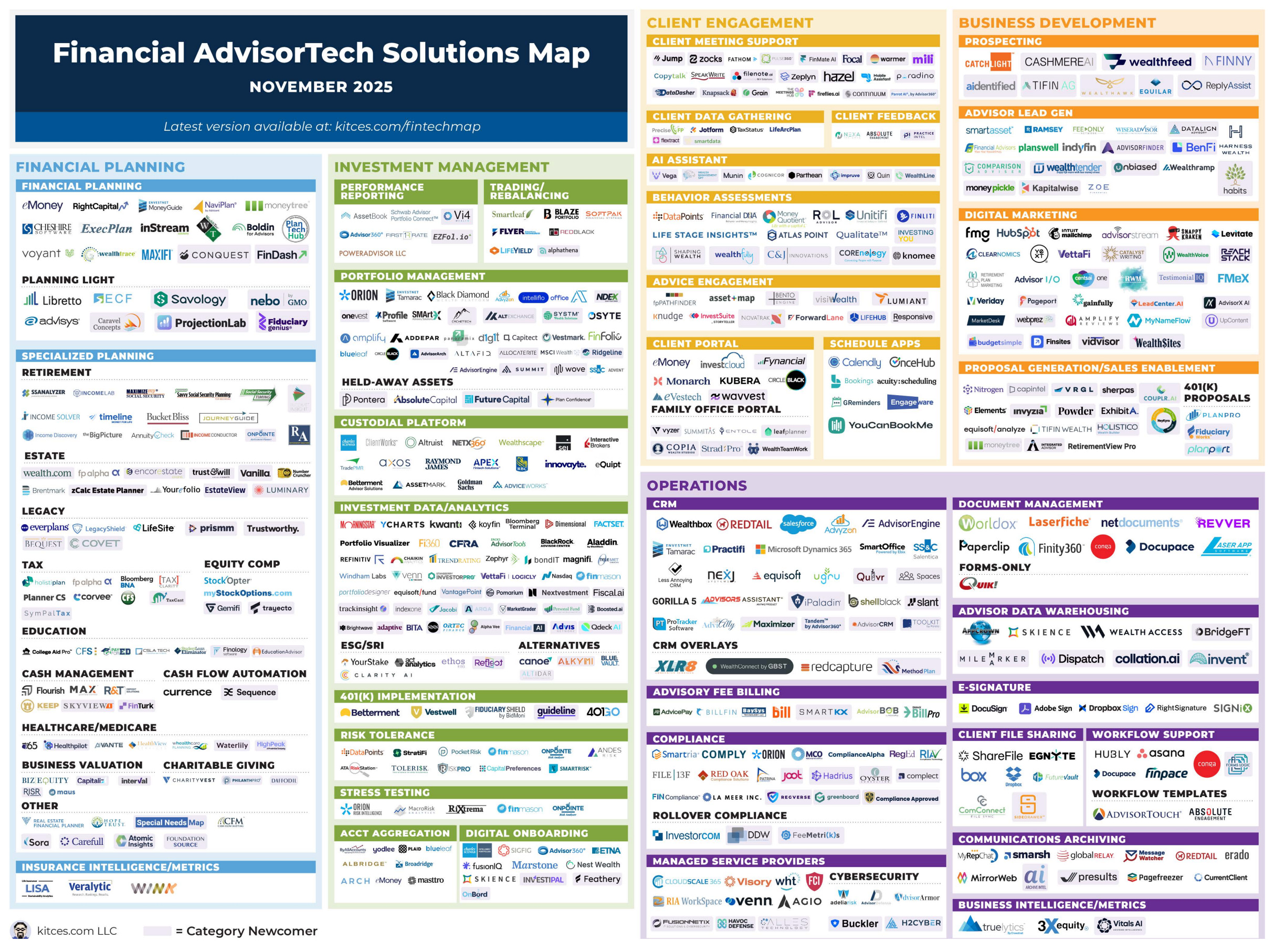

Wealth management collectively oversees $145 trillion in client assets. Most firms do it with twelve logins, an Excel sheet, and a prayer - which, as the latest Kitces data confirms,1 is about the median tech stack.

Over the past two decades, the industry has seen an explosion of specialized software: CRMs, planning tools, portfolio systems, rebalancers, client portals, compliance platforms. The most recent wave - AI-enabled note-takers, meeting summarizers, and CRM assistants - follows the same pattern: new tools grafted onto old workflows.

On paper, the ecosystem looks mature. In practice, it’s less of an ecosystem and more of a series of data handoffs. No wonder integration tops every advisor’s wishlist, even as only one in ten firms reports fully integrated workflows.2

In reality, advisors spend their days jumping between systems that don’t talk to each other, reconciling data that never quite matches, copying the same details into five different places. The software stack got deeper, but the work didn’t get easier: it just scattered.

Everyone agrees that the single most important job of an advisor is to build and maintain trust with clients, yet much of an advisor week goes to administrative work.3

It’s not inefficiency at the margins; it’s structural drag baked into the operating model.

What keeps advisors from spending time with clients isn’t the absence of a smarter app. It’s the absence of a system that holds context together - an operating system for wealth management.

Context Loss

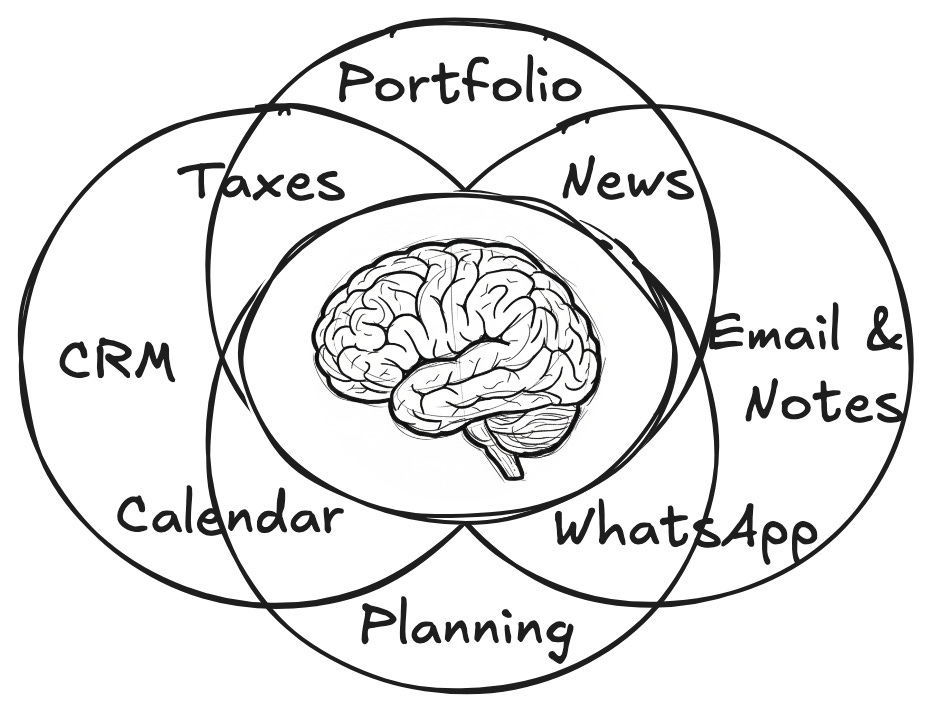

Wealth management’s core systems have one shared flaw: they don’t remember what they learn. Advisors call it by different names - missing data, out-of-sync systems, messy CRMs. I call it context loss.4

At the core of context loss is that information about a family’s life, goals, income history, assets, risk, taxes, and preferences lives in different silos, each with its own partial version of truth:

The CRM knows who the client is

The portfolio management system knows what they own

The planning tool knows what they want

Emails and meeting notes know how what they want has changed over time

Custodians know where their assets sit

Tax filings know the trajectory of income and wealth over time

Compliance archives know what was said and when

And somewhere in between, newspapers, Wallstreetbets, and CNBC pundits still insist they know where the markets are going

Each piece knows something, but none know each other.

So firms compensate with meetings, manual work, Excel, and sometimes even project management software or knowledge managers - a fragile web of human context-holding. The real system of record isn’t digital at all; in most firms it’s the advisor’s brain. They carry the context in their heads because nothing else does.5 That model doesn’t scale, and it doesn’t adapt.

This is the architectural flaw that underlies nearly every operational pain point in wealth management.

How Industries Find Their Operating System

The first operating systems, built in the 1950s by engineers at General Motors and IBM, managed how programs accessed shared hardware. By creating a common language for memory, storage, and processes, they unlocked everything that followed - personal computers, networks, and modern software.

Since then, the same principle has quietly reshaped many industries. As complexity grows, somebody eventually builds an operating layer that unifies it:

Rippling (https://www.rippling.com/) does this for HR and IT, turning payroll, onboarding, and device management into one continuous system.

Atlassian (https://www.atlassian.com/) built it for software teams, where issues, documentation, and code reviews all live in one connected workflow.

Flexport (https://www.flexport.com/) brought it to global trade, orchestrating freight, customs, and logistics data through a single platform.

Toast (https://pos.toasttab.com/) arguably does it for restaurants, merging POS, payments, and inventory into one operating backbone.

Or, put differently: When tools proliferate and coordination costs rise, industries start building connective tissue.

Wealth management has yet to reach that stage, though the forces that will force the convergence are already observable.6 But for now, the industry remains a federation of specialists - portfolio managers, planners, accountants, compliance officers, estate lawyers - each with their own systems and workflows. And unlike in hedge funds and other large institutional asset managers, the economics of most firms don’t support large internal engineering teams that could build a truly connected stack in-house.

Connected Intelligence

The first wave of AI in wealth management has shown up as digital assistants — notetakers,7 meeting summarizers, and AI-enabled CRMs.8 They add convenience but leave the underlying structure of work untouched. The same systems, the same steps - just each one done a little faster. I’d call these tools AI-enabled, not AI-native.

So what’s the difference?

AI-enabled tools layer intelligence on top of existing workflows. They enhance isolated tasks - drafting an email, summarizing a meeting - but the core process stays the same. Data still moves manually between silos. Context still depends on people remembering where things live.

AI-native platforms are built around a core of connected data. Intelligence in this context simply means that data and relationships are linked - continuously, contextually, and in real time. These systems learn from how a firm operates, adapt as new information enters, and work across connected data rather than isolated applications. They don’t automate around people; they give the system the ability to understand relationships - between clients, portfolios, communications, and decisions - as they evolve.

In practice, that means an AI-native system could, for instance, connect a client’s updated goals in a planning document to portfolio adjustments and compliance notes automatically, without anyone having to trigger the handoff. The underlying data becomes connected, not just processed.

In wealth management, that shift is still forming. I’m bullish on early signs of what comes next, after the AI notetakers and CRM assistants - the first real attempts to rebuild the system around connected intelligence.

Thanks for reading. In Part 2, I’ll dive into the horizontal and vertical dimensions of wealth management - how context moves (or fails to) through the client lifecycle and across domains like tax, estate, and investment.

If you’d like that post to land directly in your inbox, consider subscribing to Unstructured Returns.

P.S. I’d be remiss not to mention that this is the future we’re building toward at my startup, Shatterpoint. Here is a 30-seconds demo shows how our AI accesses documents in a secure vault, structures, and organizes the data, and makes it actionable through AI agents, in this case preparing for a client meeting:

I’m working with forward-thinking RIAs, multifamily offices, and wealth management firms that see AI not as hype, but as infrastructure for the next generation of advice. If this resonates, reach out - I’d love to compare notes.

According to the Kitces Report, Sept 2025, the median advisory firm uses 12 separate technology applications. But why stop at 12 when you could have 120? Kitces latest market map has got you covered.

The same Kitces Report finds that integration tops advisors’ tech wishlists, yet fewer than 10% of firms report “fully integrated workflows” (p. 16).

Across firms, advisors report spending roughly 25–30 hours per week on administrative tasks - moving data between systems, formatting reports, and documenting interactions. Meeting prep alone averages 4–6 hours per client, while compliance adds another 200 hours annually per firm.

Context here refers to the continuity of client information across systems - not the AI definition of model context windows or persistent agent memory. The two intersect, but they aren’t the same thing.

In another corner of finance - risk management - quants define key person dependency as the concentration of critical knowledge, decision-making, or client relationships in a single individual. It’s why measures like succession planning, team redundancy, and even “garden leave” exist: to reduce disruption or information leakage when key talent walks out the door.

The continued rise of retail assets, the great wealth transfer, fee compression, and the maturity of AI. I’ll save that for another post.

For a deeper discussion, see “The Future of the CRM as a Second Brain” on YouTube

Excellent writeup!!