The Missing Layer - Part 2: Reconstruction

Wealth Management Needs an Operating System, Not Another Tool

This is the second of two essays on why wealth management needs an operating system, not another tool. Part 1 traced how fragmentation and “context loss” became structural. Part 2 looks at what reconstruction requires - across workflows, across domains, and across the architecture itself.

The Horizontal Dimension

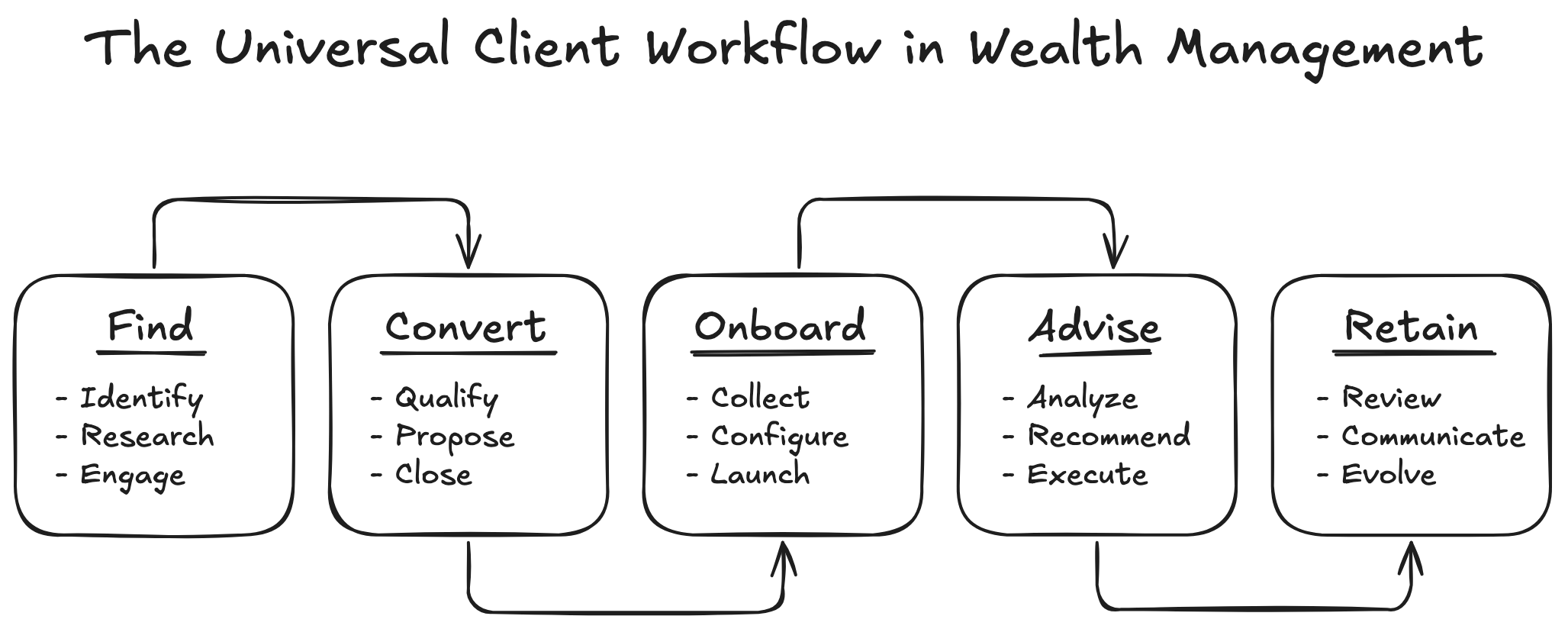

Every RIA and family office, no matter its size or philosophy, runs on the same underlying sequence: find clients, convert them, onboard them, advise them, retain them. Growth depends on how efficiently a firm can move through that loop - and how well it maintains context1 from one stage to the next.

That’s harder than it sounds.

Here is a version of what happens every day inside most firms: A prospect becomes a client, but the details gathered during discovery live in a form or an email thread that never makes it into the CRM. A portfolio is implemented, but the reasoning behind specific decisions - why this allocation, why now - is buried in a note or forgotten after the next rebalance. The client’s long-term goals live in a planning tool that nobody opens again until renewal season.

This is an architecture problem, though it often makes people feel as if they’re unorganized or careless when they’re not. Each step of the workflow is served by a different system, optimized for its own function but blind to what came before or after. Information that should flow horizontally through the client lifecycle instead falls through the gaps between tools.

When I ask firms what differentiates them, the answers often map neatly onto this workflow. For example, some excel at the early stages - finding and converting clients through sharp marketing and fast onboarding - but struggle with personalization once portfolios are implemented. Others are outstanding at managing and retaining clients, often through sophisticated investment or planning work, but rely heavily on referrals because the front end of the funnel isn’t built to scale.

It’s the same system, fractured in different places.

A true operating layer - one built on connected data - wouldn’t erase those differences, but it would preserve continuity. Context would follow the client from prospect to portfolio review without needing to be manually reassembled at every step.

The Vertical Dimension

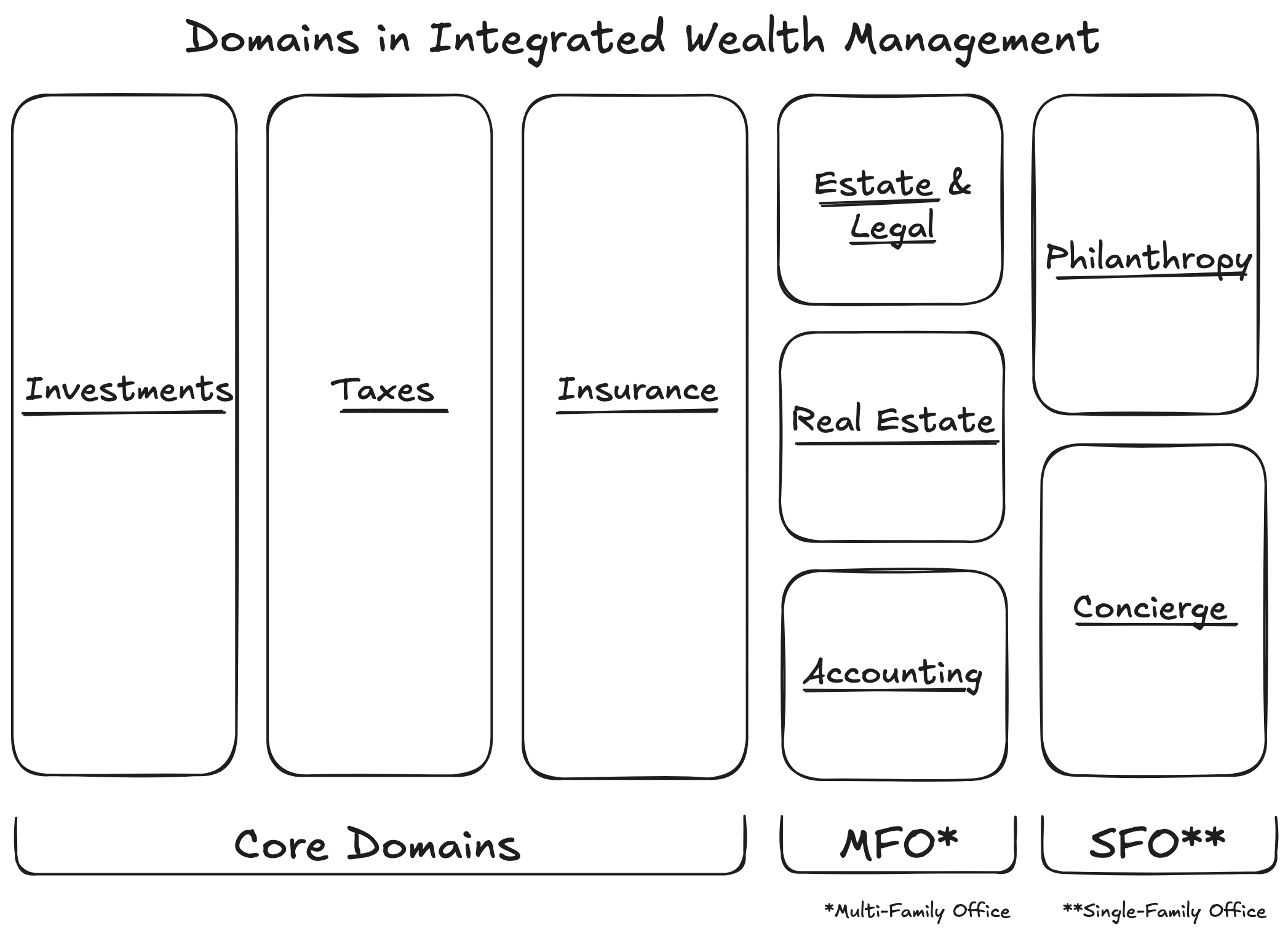

The second axis of fragmentation in wealth management runs vertically - across domains that should work together to cover all aspects of a family’s or household’s wealth. Conceptually, wealth management ties together three kinds of capital: financial capital, structural capital, and human capital.2

Core domains include investments, tax, and insurance advisory. Depending on the size and complexity of a client’s situation, these expand to estate and legal structures, real estate, accounting for owned businesses, and philanthropy. Some family offices extend even further into lifestyle management - travel, concierge, or education services - though these reinforce relationships more than architecture.

Each domain is its own discipline, with its own systems, data models, and language. Together, they form the vertical stack of modern wealth management.

In theory, these domains are interdependent. In practice, they operate in silos.

The portfolio team makes allocation decisions without seeing real-time tax implications. Accountants discover the impact months later. Estate planners work from static snapshots that rarely reflect current holdings. Insurance strategies get updated in isolation, disconnected from investment or liquidity planning.

Even firms that claim to offer all these services “under one roof” usually connect them through people, not systems. Advisors, accountants, and lawyers exchange PDFs, not data. The integration is manual - meetings, spreadsheets, and shared folders standing in for what could, and probably should, be structural coherence.

I’m not a historian of wealth advisory, but my guess is that each domain evolved its own regulatory regime, professional culture, and technology stack. Integration was technically complex and financially prohibitive, so specialization became the default. The costs of that setup are felt both in the fees paid to external service providers and in the coordination and friction required to hold it all together.

A true operating layer wouldn’t flatten these disciplines or replace expertise. It would connect them. Each domain would remain distinct but operate from shared context — so that a portfolio adjustment, a tax projection, and an estate update all draw from the same source of truth.

Where the Puck is Going

The fragmentation we live with made sense in a pre-AI world. When systems couldn’t reason, specialization was the only way to scale. Each function built its own stack - investment, tax, planning, compliance - because that was the only model technology could support.

That logic no longer holds.

Three forces3 are reshaping the field at once:

Client expectations are rising as personalized portfolios and direct indexing move from the ultra-wealthy into the mass-affluent market.

Operational complexity is breaking the traditional advisory model as firms juggle more data, regulation, and client demands with fewer people.

And for the first time, AI has matured beyond experimentation. It’s ready to deliver connected insight, dynamic goal tracking, and real-time personalization at scale.

What makes this moment different is that the technical foundation has finally shifted. Under the hood, we now have systems that can retrieve information semantically, understand relationships through graph-based models, operate through agentic workflows, and reason over real-time data. In other words, the technical constraints that forced wealth management into silos for decades are dissolving.

As AI becomes more reliable - grounded in connected data rather than isolated applications - the architecture of wealth management has to change. Software can no longer stop at recording transactions any longer. It has to understand relationships - across workflows and across domains. And we’re already seeing early signals of that shift: index construction becoming programmable,4 client acquisition becoming automated,5 and intelligent agents quietly coordinating data across tools.6 These aren’t features. They’re the beginning of a structural shift.

In wealth management, that shift won’t require redesigning workflows, but making technology flexible enough to follow them. Conversational interfaces and contextual intelligence allow systems to meet advisors where they are, not the other way around.

Once that happens, the experience of working inside a firm changes.

This will make possible an advisor workspace where context finally lives in the infrastructure - remembered, linked, and updated automatically instead of manually reconstructed each day. A preference mentioned by a client is immediately translated into a personalized investment recommendation. A portfolio adjustment informs a tax projection. A liquidity event updates an estate plan. A client note syncs automatically with the CRM.

The technology to build this kind of system - what I call an AI-native Operating System - already exists. And to be clear, this shift isn’t about disrupting the industry or replacing the advisor. It’s an architectural correction - the moment when wealth management technology starts to operate as one connected system rather than a set of parallel ones.

Call it connective intelligence, contextual infrastructure, or simply the next operating layer. The name matters less than the direction: once systems can understand context, fragmentation stops making sense.

Thanks for reading. If this resonated, feel free to share it with anyone working in wealth management or thinking about how the industry is changing in the age of AI.

Unstructured Returns covers the intersection of startup, AI, finance, and the systems that sit underneath them. If you’d like future pieces to land directly in your inbox, consider subscribing.

P.S. If you’re interested in what this looks like in practice: this is the future we’re building toward at my startup, Shatterpoint. Here is a 30-seconds demo shows how our AI accesses documents in a secure vault, structures, and organizes the data, and makes it actionable through AI agents, in this case preparing for a client meeting:

I’m working with forward-thinking RIAs, multifamily offices, and wealth management firms that see AI not as hype, but as infrastructure for the next generation of advice. If this resonates, reach out - I’d love to compare notes.

I should say that “context” has a precise meaning in AI, and I’m using it differently here. In this piece it’s about the continuity of client information across systems, not model context windows or persistent agent memory. These two meanings two intersect, but they aren’t the same thing.

There are several ways to categorize the forms of capital that underpin family wealth. PwC’s Global Family Office Deals Study 2025 (link) implicitly distinguishes three:

Financial capital - the money side, i.e. investments, accounting, capital

Structural capital - how wealth is held, i.e. legal, real estate, business ownership

Human capital - who it is for and how it is stewarded, i.e. through family office services, governance, succession, education

Pathstone, a U.S.-based multi-family office and advisory firm, defines five types: financial, human, relationship, legacy, and social capital (link)

The three forces will get their own post later. In the meantime, several industry reports describe the same underlying trends:

McKinsey’s Asset Management 2025: The Great Convergence (link) notes rising expectations for personalization and digital client experiences extending beyond UHNW clients into the mass affluent segment, alongside mounting operational complexity from regulation and data volume.

PwC’s Asset and Wealth Management Revolution 2024 (link) highlights similar pressures from expanding mass affluent demand for customized portfolios such as direct indexing, forecasting consolidation and AI adoption as key enablers of scale and efficiency.

Deloitte’s 2026 Banking and Capital Markets Outlook (link) emphasizes how AI has matured from experimentation to core advisory workflows, enabling connected insights, dynamic goal tracking, and deeper personalization.

Schwab’s 2025 RIA Benchmarking Study (link) echoes these themes, pointing to workload and compliance challenges that make automation and AI-driven personalization essential to sustain service quality.

Check out Panta (https://pantaindex.com/), where Toby, Mark, and their team are pushing the frontier of index construction. Their model lets creators design index logic directly - shifting the IP of index-aligned products from manufacturers like MSCI, S&P Dow Jones, FTSE Russell to the people who define the idea. In the wealth management context, this moves direct indexing beyond tax optimization and into true product creation.

Tools like Clay (https://www.clay.com/ ) or Dripify (https://dripify.com/) show what automated client acquisition can look like when prospecting, enrichment, and outreach are linked into one intelligent workflow.

Platforms like Orkes (https://orkes.io/) demonstrate how event-driven orchestration and agent workflows are becoming real infrastructure, quietly coordinating data and decisions across tools.